Global Logistics Update

U.S. and U.K. Will Sign Trade Deal; De Minimis Expiration Creates Volatility

Updates from the global supply chain and logistics world | May 8, 2025

Global Logistics Update: May 8, 2025

May 8, 2025

Trends to Watch

Talking Tariffs

We launched the Flexport Tariff Simulator. Estimate and forecast tariffs and landed costs for each shipment, all based on real-time data and the latest rates and regulations.

U.S. and U.K. Reach a Trade Agreement: This morning, President Trump stated that the U.S. has reached a trade agreement with the U.K.—the first deal the U.S. has announced since introducing sweeping tariffs earlier this year. Per the deal, the U.S. will reduce auto, steel, and aluminum tariffs on the U.K., while the U.K. will reduce non-tariff barriers to U.S. beef, ethanol fuel, machinery, and other products.

- The 10% baseline reciprocal tariff will remain in place on all U.K. imports.

- U.K. automakers will be granted a lower-tariff quota: each year, the first 100,000 British vehicles imported into the U.S. will be subject to only the 10% baseline tariff, rather than the existing 27.5% tariff on U.K. autos.

- Tariffs on U.K. steel and aluminum will be reduced from 25% to 0%.

The timeline for implementing the deal is currently unclear, as U.S. and U.K. officials still need to finalize the specifics of the agreement.

De Minimis Exemption Expires for China/Hong Kong Imports: Just after midnight on May 2, the de minimis exemption—which allows shipments under $800 to enter the U.S. duty-free—expired for Chinese-origin imports. Effective May 2, shipments under $800 from China/Hong Kong are subject to the following fees:

- Parcel: 145% baseline tariff, along with product-specific tariffs

- Postal: 120% baseline tariff or a $100 (increasing to $200 on June 1) flat fee per postal item

Additionally, de minimis will be eliminated for all other countries once “adequate systems are in place.”

U.S.-China Trade Negotiations to Begin This Week: U.S. Treasury Secretary Scott Bessent and U.S. Trade Representative (USTR) Jamieson Greer will meet with Chinese Vice Premier He Lifeng in Switzerland between May 9 and 12, marking the first in-person negotiations between the U.S. and China since trade tensions escalated in March. Bessent does not anticipate that the U.S. and China will reach a trade deal during this meeting, but stated that “we’ve got to de-escalate before we can move forward.”

Foreign Films Face a 100% Tariff: On Sunday (May 4), President Trump announced on Truth Social that he would immediately begin the process of implementing a 100% tariff on all movies produced abroad. Anything involving filming in a foreign country—including a large portion of independent movies and streaming content—would be subject to the new tariff.

Potential Pharmaceutical Tariffs Around the Corner: On Monday (May 5), President Trump stated that he will announce pharmaceutical tariffs “over the next two weeks,” and signed an executive order containing several initiatives intended to boost domestic prescription drug manufacturing.

For the latest updates and guidance on U.S. tariffs and trade, visit our live blog.

Ocean

TRANS-PACIFIC EASTBOUND (TPEB)

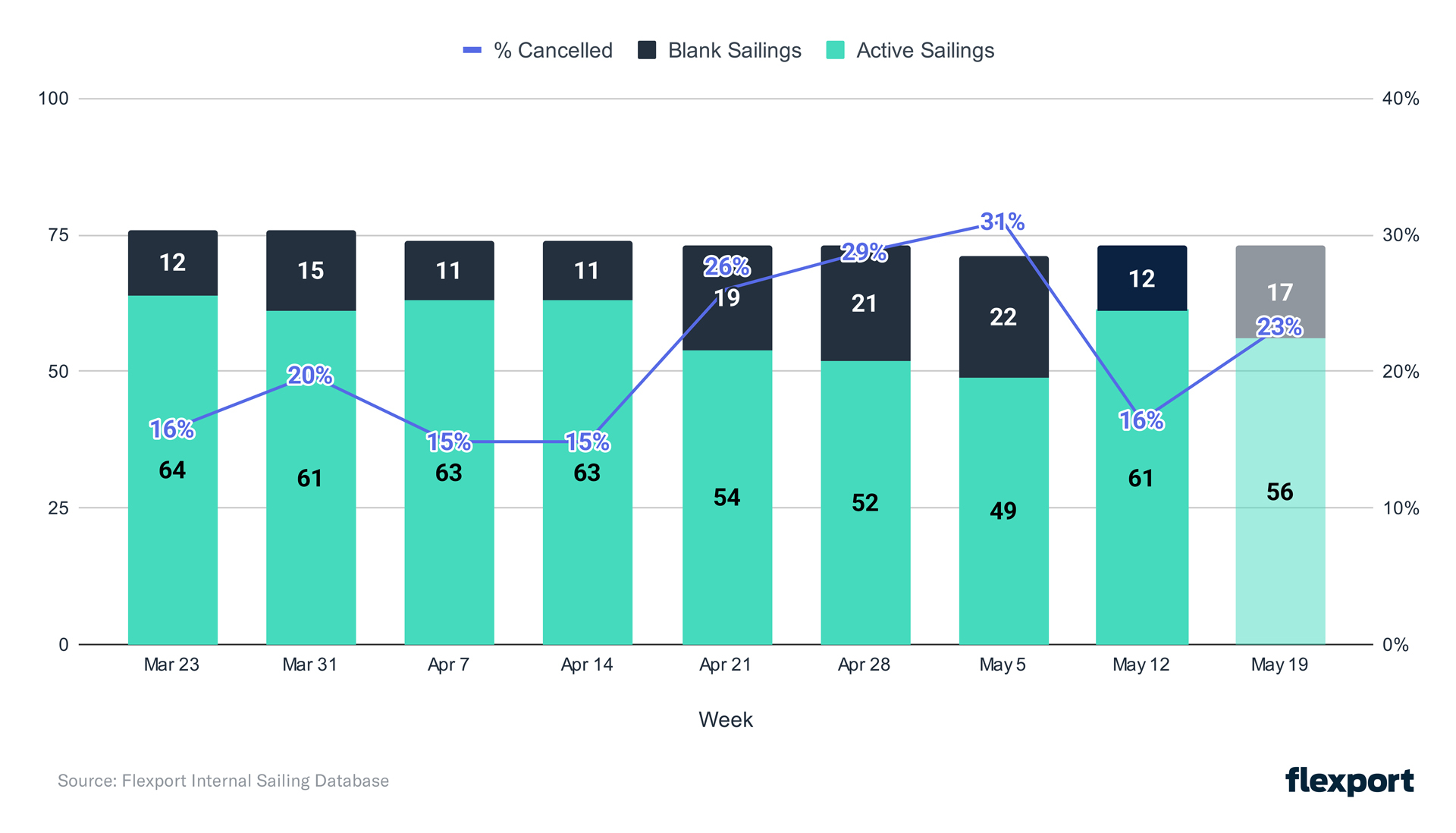

- Capacity and Demand: In both Weeks 18 and 19, offered capacity on the TPEB was about 16% below standard levels. This is driven by significant declines in demand, along with subsequent blank sailings from China to the U.S. Since Week 17, however, demand from China has not declined further, and there still have not been any notable demand increases from Southeast Asia.

- While we see an improvement in blank sailings next week (the week of May 12), we don’t anticipate it to be a sustained improvement, given that the cancellation rate is already 23% for the following week (the week of May 19). See the graph below.

The recent uptick in active sailings is due to timing fluctuations from blank sailings—some departures were skipped earlier and bunched up last week, creating a temporary spike. Looking at deployed capacity, we see future departures will continue sliding, both on actual cargo shipped and the number of vessels departing.

There are 10 service loops that have been suspended, either temporarily or indefinitely. Ocean Alliance (CMA CGM, COSCO, Evergreen, and Orient Overseas Container Liner), Premier Alliance (ONE, HMM, YML), and ZIM/MSC have completely suspended 10 of their weekly service loops. See Table 1 below for current suspensions, and check out our blog post for more details.

Table 1: Suspended Transpacific Eastbound Service Loops

| Carrier / Alliance | Service Loop | Suspension Period |

|---|---|---|

| Ocean Alliance | PRX / CP1 / PCS1 / PRX / AAS2 | Week 17 - 26 |

| Ocean Alliance | SEA3 / PSX | Week 18 - 23 |

| Ocean Alliance | CPS / AAC2 / HBB / PCN3 | Week 17 - 21 |

| Ocean Alliance | CBX / ECC3 / AWE7 / CBX | Week 16 - 24 |

| Mediterranean Shipping Company | ORIENT | Week 16 until further notice |

| ZIM | ZX2 | Week 16 until further notice |

| Premier Alliance | PN4 | Scheduled to begin in May, suspended until further notice |

| Premier Alliance | PS5 | Scheduled to begin in May, suspended until further notice |

| Mediterranean Shipping Company / ZIM | PELICAN / ZSL | Week 19 until further notice |

| Mediterranean Shipping Company / ZIM | EMPIRE / ZNS | Week 20 until further notice |

- Equipment: Currently, the overall availability of equipment (all size containers) is sufficient. There are no significant concerns about shortages at this time.

- Freight Rates: Most carriers announced General Rate Increases (GRIs), effective May 1. These GRIs have been successfully implemented.

FAR EAST WESTBOUND (FEWB)

Capacity and Demand:

- North Europe imports declined 2.4% YoY in Q1 2025 (source: Alphaliner), reflecting subdued consumer spending.

- Despite minor seasonal restocking activity in early May, European retail demand remains stagnant due to inflationary pressures (with the Eurozone CPI at 3.1% YoY) and weakened purchasing power.

- Oversupply continues; carriers will intensify capacity cuts by maintaining blank sailings. Sea-Intelligence indicates that May blank sailing ratios on the FEWB may surge to 12-15%, exceeding initial projections of 8-10%.

- North European hubs (Rotterdam, Hamburg) face 5-7-day berthing delays, per Sea-Intelligence, due to labor shortages and vessel bunching. This will impact operational efficiency and vessel turnaround times.

Freight Rates:

- The Shanghai Containerized Freight Index (SCFI) has shown a gradual decline, with recent weeks indicating a decrease. Since this year’s peak (to date) in Week 11 of $1,582, the SCFI has decreased by 24%—now at $1,200 in Week 19.

- Core carriers like MSC and CMA have announced a slight reduction in FAK rates for the second half of May, reflecting a strategic approach to maintaining market share and encouraging cargo bookings.

- Rates are expected to stabilize in the short term, with limited further drops due to balanced capacity adjustments and carrier rate strategies.

TRANS-ATLANTIC WESTBOUND (TAWB)

- Capacity and Demand: Congestion persists at the Ports of Piraeus, Genoa, and Valencia in the Mediterranean, and in Hamburg, Bremerhaven, Rotterdam, and especially Antwerp in North Europe. This has led to delays and is negatively affecting schedule reliability. Blank sailing numbers have decreased.

- Equipment: Equipment shortages persist in parts of Central Europe, particularly in Austria, Slovakia, Switzerland, Hungary, and Southern/Eastern Germany. Carrier haulage is recommended for these origins. No major issues in other ports and regions.

- Freight Rates: Due to the postponement of U.S. tariffs in the EU, carriers are anticipating a peak in demand for the next 90 days. Vessel utilization is good but not overbooked, which forces carriers to reconsider if this peak in demand will happen.

- North Europe: Carriers have postponed their May Peak Season Surcharge (PSS) until June.

- West Mediterranean: Carriers have postponed the PSS until the end of June.

- East Mediterranean: With demand expected to be higher, carriers are considering postponing their PSS until June and re-evaluating the situation.

INDIAN SUBCONTINENT TO NORTH AMERICA

- Capacity and Demand: Capacity is largely stable following multiple blank sailings in April. Demand is expected to increase in the coming weeks as shippers look to pull forward cargo before higher tariffs are implemented.

- Equipment: No major equipment issues have been reported. But with changes of services related to the ongoing Pakistan-India conflict, we can expect a lack of equipment in the coming weeks in Pakistan, which is susceptible to equipment issues.

- Freight Rates: In the second half of May, freight rates will increase alongside rising demand to beat the expected hike in tariffs following the 90-day pause.

Air

WEEK 17: APRIL 21 - APRIL 27, 2025

- +6% YoY Global Tonnage Growth in April: Growth was led by the Asia-Pacific (+10%), with U.S. importers ramping up air freight ahead of May 2 changes to China–U.S. de minimis rules and aiming to avoid new tariffs and customs costs.

- Mixed Month-on-Month Performance: Despite YoY gains, April volumes dropped vs. March across most regions (e.g., Europe -10%, MESA -12%), except for Central & South America (+16%), fueled by Mother’s Day flower exports.

- Rates Stable at $2.43/kg, Globally: But China–U.S. spot rates fell from $5.63 to $4.18/kg in two weeks, signaling the end of pre-loading activity as well as weakening demand after seven weeks of rate surges.

- Major Volatility Expected Post-May 2: Given the end of de minimis, air freight flows from China/Hong Kong to the U.S. could see a sharp drop. Freighter aircraft may continue to shift to other lanes, and spot pricing is likely to fluctuate.

Source: worldacd.com

Please reach out to your account representative for details on any impacts to your shipments.

North America Vessel Dwell Times

Upcoming Webinars

Tariff Trends 2025: Expert Insights on the New U.S. Customs Landscape

Thursday, May 15 @ 8:00 am PT / 11:00 am ET / 16:00 BST / 17:00 CEST

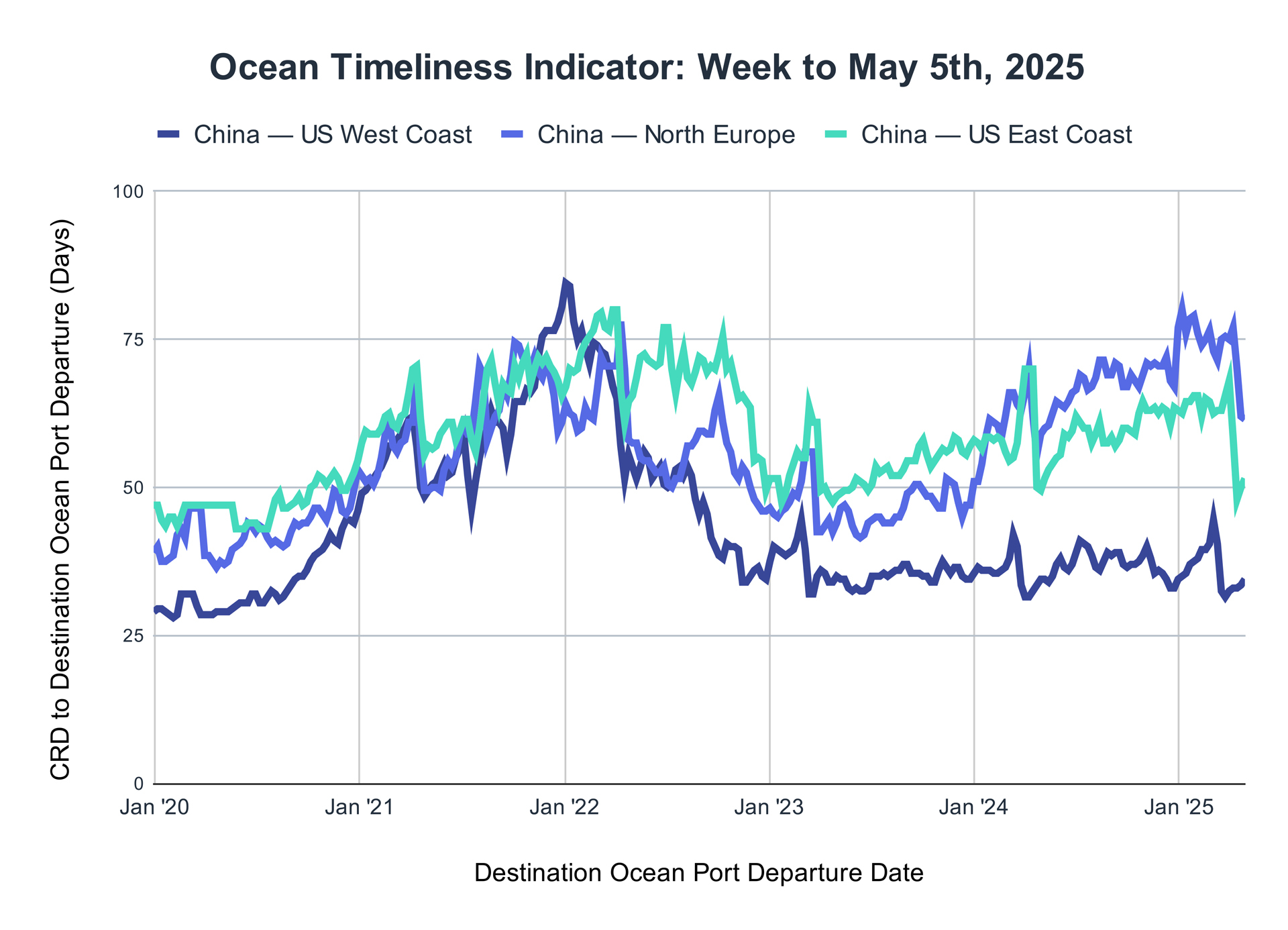

Ocean Timeliness Indicator

This week, the Flexport OTI for China to the U.S. West Coast and China to the U.S. East Coast showed a small uptick. Meanwhile, China to North Europe dropped by half a day.

Week to May 5, 2025

The Ocean Timeliness Indicator (OTI) demonstrated minor fluctuations this week, with China to the U.S. West Coast increasing by a day to 34.5 days. Meanwhile, China to the U.S. East Coast showcased a similarly small uptick, increasing from 50 to 51.5 days. China to North Europe has finally shown signs of stabilization, falling only by half a day from 62 to 61.5 days.

About the Author

May 8, 2025

Sign up for Global Logistics Update

Why search for updates when we can send them to you?

Related content

More from Flexport

![Ocean Port GettyImages-89849286]()

Global Logistics Update

CIT Orders IEEPA Tariff Refunds; Middle East Escalation Disrupts Air and Ocean Operations

![GettyImages-1295614211]()

Global Logistics Update

Prepare for Potential IEEPA Tariff Refunds; U.S. Blizzards Disrupt Europe and North America Air Freight Operations

![WarehouseGettyImages-535667233]()

Global Logistics Update

U.S. and Taiwan Finalize Trade Deal; FEWB Spot Rates Soften Amid Lunar New Year Lull

Ready to get started?

Learn how Flexport’s supply chain solutions can help you capture greater opportunities.