Global Logistics Update

Steel and Aluminum Tariffs Double to 50%; Capacity Tightens on TPEB and FEWB

Updates from the global supply chain and logistics world | June 5, 2025

Global Logistics Update: June 5, 2025

June 5, 2025

Trends to Watch

Talking Tariffs

This week, we launched the Flexport Tariff Simulator. Estimate and forecast tariffs and landed costs for each shipment, all based on real-time data and the latest rates and regulations.

- Steel and Aluminum Tariffs Rise to 50%: On June 3, the Trump administration released a proclamation that raises the duty rate on steel and aluminum articles and derivatives from 25% to 50%, effective June 4 at 12:01 a.m. ET. Other highlights of the proclamation include:

- Great Britain is exempt from this tariff increase, per the U.S.-U.K. Economic Prosperity Deal (EPD). However, the 25% duty rate may rise after July 9 if the U.K. does not meet EPD conditions.

- Steel and aluminum imports from Mexico and Canada are also subject to the new 50% duty rate, even if those goods are claimed under the United States–Mexico–Canada Agreement (USMCA). Additionally, the stacking order of Mexican and Canadian goods has been modified: Section 232 duties now apply in place of IEEPA tariffs.

- Reciprocal tariffs now apply to non-steel and non-aluminum content.

- U.S. Customs and Border Protection (CBP) will issue authoritative guidance mandating strict compliance and outlining maximum penalties for non-compliance.

- CBP Updates Guidance on In-Transit Exception to IEEPA Reciprocal Tariffs: On May 30, CBP announced that the window for shipments to qualify for in-transit exceptions to reciprocal tariffs would be extended to June 16, 2025.

- Previously, shipments needed to be loaded onto the final ocean vessel and in transit to the U.S. prior to April 5, April 9, or April 10, depending on the applicable in-transit exception, and arrive by May 27.

- Per CBP’s updated guidance published on May 30, however, goods may qualify for in-transit exceptions if they “are entered for consumption, or withdrawn from warehouse for consumption” before June 16.

- IEEPA Tariffs Remain in Place While Court Reviews Proceed: On May 29—less than a day after the Court of International Trade (CIT) invalidated four of President Trump’s IEEPA tariff orders—the U.S. Court of Appeals granted a temporary stay, enabling IEEPA tariffs to remain in effect.

- According to the stay, the plaintiffs have until June 5 to respond, and the government until June 9.

- The losing side will likely appeal to the Supreme Court. A final decision on the tariffs may take months, but given the national importance of the case, resolution may come sooner.

Get the latest updates and guidance on U.S. tariffs and trade on our live blog.

Ocean

TRANS-PACIFIC EASTBOUND (TPEB)

- Capacity and Demand:

- Increasing Volume: Demand remains strong, with volumes continuing to surge into June.

- Potential Rush from Southeast Asia: With shippers looking to move cargo before the end of the 90-day country-specific reciprocal tariff pause on July 9, we anticipate a further rush of cargo from Southeast Asia to the U.S. West Coast toward the end of June.

- Capacity Restoration: Carriers are actively working to restore capacity, with full capacity expected to return by the end of June. This week (Week 23), offered capacity on the TPEB is 11% below standard levels, and is expected to exceed standard levels by 3% in Week 25.

- Current Utilization: For the month of June, average capacity on the trade is expected to be above 85% of planned. Vessels are sailing full.

- Blank Sailings: Sailing cancellations continue to decline as carriers bring previously announced sailings back online. This week, we saw a cancellation rate of 13% (a 62% decline vs. the week of May 5). Next week (June 9), blank sailings are forecasted to improve further, with a projected cancellation rate of just 9%.

- Extra Loaders and Resumed Services: Multiple carriers have deployed extra loader vessels and resumed previously suspended services to meet increased demand. A total of seven out of ten previously suspended service loops have either already resumed, or are scheduled to resume in the coming weeks. See our blog for detailed updates on blank sailings and service resumptions.

- Given increased demand, vessel capacity is being booked up. Shippers are advised to book 4 weeks in advance, and use premium options if urgency is a priority. Reach out to your Flexport representative for more information on premium options.

- Equipment: Equipment availability generally remains sufficient, and container shortages are not an immediate concern.

- Freight Rates:

- General Rate Increase (GRI) and Peak Season Surcharge (PSS) Implementation: The GRIs and PSSs for June 1 have been implemented. For the June 15 GRI, some carriers may extend West Coast gateway rates until the end of June, while maintaining the GRI for the East Coast.

- Factors Driving Increases: The firm implementation of these rate increases can be attributed to surging demand, coupled with capacity that has not yet fully recovered on the TPEB market, affecting both floating (spot) and fixed rates.

FAR EAST WESTBOUND (FEWB)

- Capacity and Demand:

- Major port congestion has resulted in long delays in both Asia (Shanghai, Singapore) and Europe (Antwerp, Hamburg, Bremerhaven).

- Supply on the FEWB has been reduced by 17%, given that some vessel capacity has been shifted away from the FEWB to the busy TPEB lane instead.

- Most carriers are already fully booked for the first half of June, with space filling up 2-3 weeks in advance.

- Cargo rollovers are increasing, and likely to impact later June sailings as well.

- When it comes to accepting bookings, carriers are currently highly selective. Last-minute options are extremely limited.

- Shippers are advised to secure space as soon as possible. Delayed bookings may result in much higher costs, or even the inability to move cargo at all.

- Freight Rates:

- The previous rate floor of around 2,100 USD/FEU no longer applies; space at that price is gone.

- The spot rate market has jumped over 23% on the FEWB, and is projected to increase even further in the coming weeks.

- Carriers have introduced additional PSSs, with rates expected to continue climbing.

- If you have upcoming shipments, share your forecasts and allocate bookings immediately. This will allow us to secure available space before rates and tightness potentially worsen.

TRANS-ATLANTIC WESTBOUND (TAWB)

- Capacity and Demand: Congestion remains at Northern European ports. In Antwerp in particular, delays have increased substantially due to recent strikes. In the Mediterranean, Piraeus is still experiencing congestion. These delays continue to impact schedule reliability.

- Equipment: Equipment shortages persist in parts of Central Europe, particularly in Austria, Slovakia, Switzerland, Hungary, and Southern/Eastern Germany. Carrier haulage is recommended for these origins. Mersin and Aliaga in Turkey and Lisbon in Portugal continue to face equipment shortages; carriers are continuing to carry out empty repositions to support demand.

- Freight Rates:

- North Europe: Carriers are postponing their PSSs until July.

- West Mediterranean: One carrier is attempting to implement a PSS for June, while the rest have postponed their PSSs until July.

- East Mediterranean: Some carriers have further postponed their PSSs until July, while others have postponed it until further notice.

INDIAN SUBCONTINENT TO NORTH AMERICA

- Capacity and Demand:

- Capacity to the U.S. West Coast is constrained due to limited direct services, which also call on Chinese and Vietnamese ports of loading, as well as increases in bookings from those regions (China and Vietnam).

- Capacity to the U.S. East Coast is greater due to numerous direct services in the market, which are Indian-subcontinent-specific ports of loading. Carriers are reporting that they are running ships fully utilized on such services.

- Freight Rates:

- For Indian subcontinent cargo moving to the U.S. West Coast, carriers have announced GRIs and PSSs for the second half of June in light of pressure on capacity stemming from booking increases from China and Vietnam to the U.S.

- For cargo moving to the U.S. East Coast, carriers have implemented GRIs and PSSs for the first half of June, which are expected to continue into the second half of June if vessels continue to be highly utilized.

- Exports from Pakistan are seeing increases due to additional feeder services being launched in light of the India-Pakistan conflict.

Air

WEEK 21: MAY 19 - MAY 25, 2025

- Global Tonnages Stable Week Over Week, but +6% YoY: Worldwide air cargo volumes held flat versus the previous week, but rose +6% year over year, with the Asia-Pacific contributing the largest absolute volume growth.

- Global Two-Week Trend Up +7% (2Wo2W): Combining the last two weeks, worldwide demand increased +7% versus the prior two weeks, driven by a strong spike in Week 20.

- Asia-Pacific–North America Lane Demonstrates Strong Rebound: Volumes rose +19% from the Asia-Pacific to North America, and +13% in the reverse direction. Meanwhile, Central and South America to North America dropped -23% due to post-Mother’s-Day flower shipment declines.

- China to the U.S. Recovers, and China to Europe Grows YoY: China-U.S. volumes rebounded from recent lows, now just -5% below 2024 levels after a -14% six-week average. Additionally, China-Europe exports grew +11% vs. 2024, despite a -3% WoW dip in Week 21.

(Source: WorldACD)

Please reach out to your account representative for details on any impacts to your shipments.

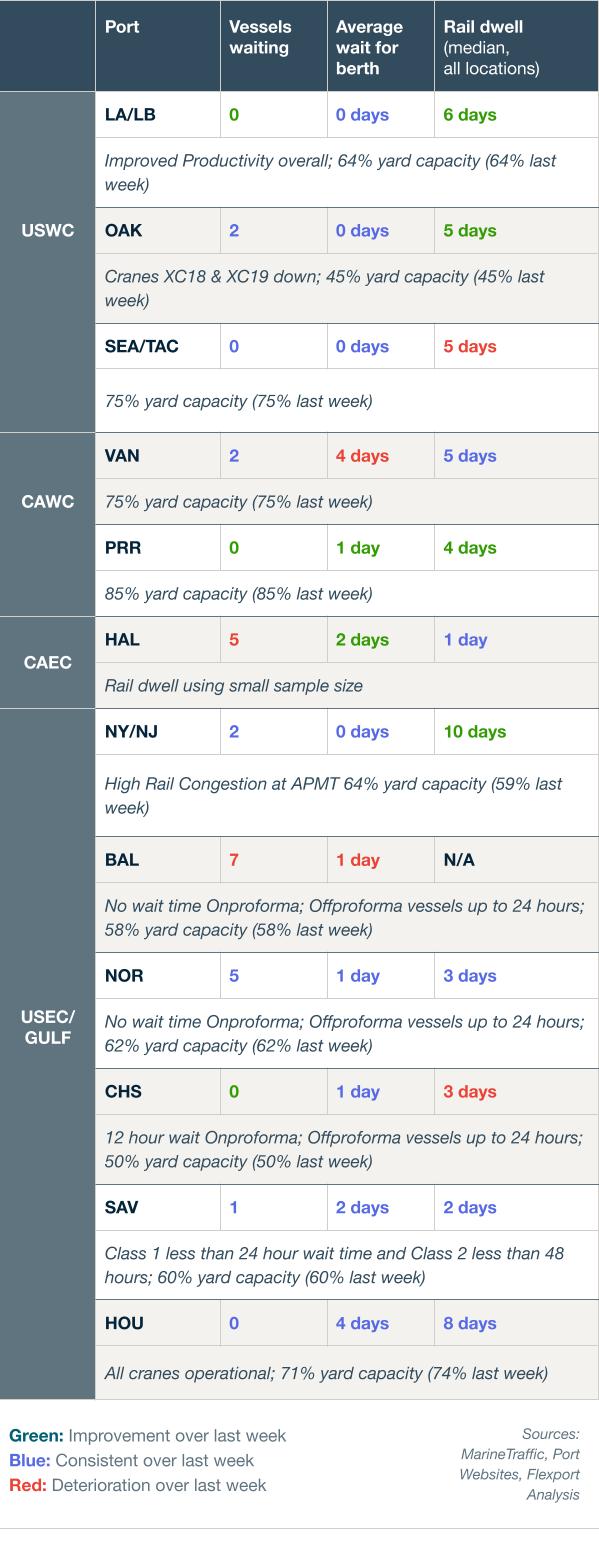

North America Vessel Dwell Times

Upcoming Webinars

European Freight Market Update Live

Tuesday, June 10 @ 15:00 BST / 16:00 CEST

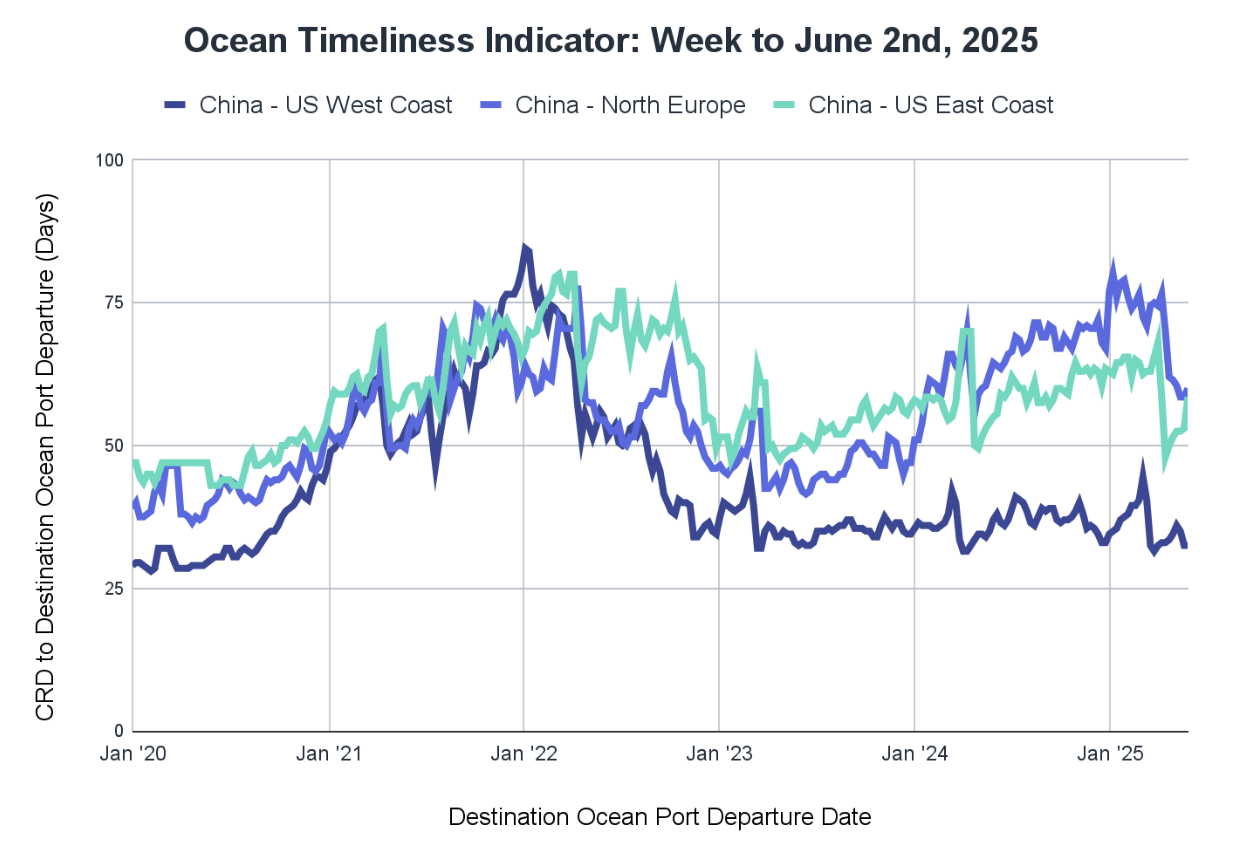

Ocean Timeliness Indicator

This week, the Flexport OTI for China to the U.S. West Coast remained stable, China to North Europe increased, and China to the U.S. East Coast jumped.

Week to June 2, 2025

The Ocean Timeliness Indicator (OTI) for China to the U.S. West Coast idled at 32.5 days. Meanwhile, China to North Europe showed a small uptick, rising from 58.5 to 60 days. The big move of the week comes from China to the U.S. East Coast, with a jump from 53 to 58.5 days.

About the Author

June 5, 2025

Sign up for Global Logistics Update

Why search for updates when we can send them to you?

Related content

More from Flexport

![Ocean Port GettyImages-89849286]()

Global Logistics Update

CIT Orders IEEPA Tariff Refunds; Middle East Escalation Disrupts Air and Ocean Operations

![GettyImages-1295614211]()

Global Logistics Update

Prepare for Potential IEEPA Tariff Refunds; U.S. Blizzards Disrupt Europe and North America Air Freight Operations

![WarehouseGettyImages-535667233]()

Global Logistics Update

U.S. and Taiwan Finalize Trade Deal; FEWB Spot Rates Soften Amid Lunar New Year Lull

Ready to get started?

Learn how Flexport’s supply chain solutions can help you capture greater opportunities.